SSSE’s core values are Fun, Integrity, Drive, and Others-First. As part of our commitment to Others-First, we strive to educate our investors, partners, and the general public about self storage. The Roman philosopher Seneca once said, “Luck is what happens when preparation meets opportunity”. This Frequently Asked Questions page is to serve as preparation for anyone interested in learning more about self storage and SSSE. The opportunities come when you sign up for SSSE’s investors list or buyers list by clicking the links in our menu bar. We hope to be lucky enough to work together.

If there are any questions that you have that are not answered below, please contact info@ssse.com

Are self storage rental rates recovering?

The rate story is not all bad, but it is not a straight-line recovery either.

From Q4 2024 to Q2 2025, rental rates increased across all unit sizes and climate types. That suggests some pricing power may be returning. But year over year, the data still showed rental rates down 1.61 percent for non-climate-controlled units and down 2.63 percent for climate-controlled units. The key takeaway: near-term improvement does not erase the broader reset from pandemic-era pricing. In some markets- primary markets for the most part- rental rates increased 7% month over month during the pandemic. That meteoric increase in rates was never going to be sustainable no matter the inflationary conditions. Buyers that bought based on those financials are now in the midst of a rude awakening as interest rates maintain elevated levels and expenses continue to rise. Investors should model modest growth, monitor concessions, and understand whether a market is improving because demand is returning or because operators finally stopped cutting rates.

Why is 90 percent occupancy not always the right assumption?

If every deal you see assumes 90 percent-plus occupancy, pause.

The state-level and non-REIT data tell a more nuanced story. Most states report occupancy between 80 percent and 90 percent, with a total weighted average of 88.3 percent. Storable’s 25,000-plus facility dataset averaged 81.8 percent over the last year. That does not mean a strong facility cannot run above 90 percent. It means buyers should not blindly assume 90 percent in every market. Stabilized occupancy depends on supply, population growth, competition, pricing discipline, management quality, and seasonality. When a facility is bought or sold, the occupancy usually takes a hit. Many of our underwrites don’t anticipate an increase in economic occupancy until after the first year because we acknowledge a stabilization phase. Some tenants will get annoyed by the transition to new management and new policies. Delinquent units may be auctioned off rather than provide phantom occupancy figures. In today’s environment, disciplined buyers underwrite a range of occupancy outcomes, not a single optimistic number.

Can discounting hide weak demand?

A facility can look full and still be buying occupancy with discounts.

Discounting is one of the easiest ways to misunderstand performance. The 2026 Self Storage Almanac shows discounting around 20 percent in 2019, rising to roughly 35 percent during the pandemic peak, dropping below 15 percent in 2021, and remaining elevated at 17.7 percent in Q2 2025. When discounts are high, the advertised rent may not reflect the real economic rent. For sellers, discount discipline can improve buyer confidence. For buyers, discounts are a diligence item: how many tenants are on promos, how long do concessions last, and what happens when those tenants roll to standard rates?

What does normal occupancy really look like?

A lot of people still underwrite self storage like it is 2021. That is dangerous.

REIT weighted occupancy peaked at 96.6 percent in Q2 2021, while non-REIT occupancy peaked at 90.0 percent. By Q4 2024, occupancy had bottomed at 90.4 percent for REITs and 80.9 percent for non-REITs. The lesson is not that storage is broken. The lesson is that pandemic-era occupancy was not normal. If a seller presents peak occupancy as stabilized performance, buyers should normalize the numbers. A good underwriting model should account for seasonality, local supply, concessions, and the difference between physical and economic occupancy. While delinquent units present an opportunity for accounts receivable, they should not be counted as normal physical occupancy. We consider any unit greater than 60+ days as a vacant unit because they are less likely to come current, and a properly followed lien and auction process will result in an empty unit within 60 days usually.

Why do construction starts matter more than headlines?

A market can look healthy today and still become risky if too much new space is already in motion.

In markets tracked by Matrix for at least 24 months, the under-construction pipeline declined 6.2 percent quarter over quarter to 49.79 million net rentable square feet and 17.3 percent year over year. That decline is encouraging, but it does not eliminate risk. Most of that inventory still needs to be delivered and absorbed. Construction starts also remain a leading indicator. If starts fall, future competitive pressure may ease. If starts rebound because rates grow and capital or construction gets cheaper, supply risk can return. For investors, the underwriting lesson is clear: do not evaluate occupancy and rent today without also evaluating what is scheduled to open tomorrow. Unless a municipality has barriers in place- such as a moratorium- an errant developer can throw a wrench into an entire market. We try to leave “meat on the bone” when looking at a market. If the equilibrium supply index for a market is 7- meaning 7 net rentable square feet per capita results in an average occupancy of 85%- we try to have the supply index come in at less than the equilibrium AFTER our development is accounted for. We’d like to see room for another 1 or 2 self storage facilities before the equilibrium supply index is hit so that we have a protective buffer to our lease up or stabilized occupancy. If we reach stabilized occupancy and there are no new developments to erode the buffer, then expansion can be considered.

Is the self storage supply pipeline slowing?

One of the biggest questions in self storage right now is simple: are we overbuilt?

The supply data shows a mixed answer. Yardi Matrix increased its Q4 2025 forecast by 4.3 percent for 2025 and 4.6 percent for 2026, bringing expected 2025 completions to 59.44 million NRSF and 2026 completions to 48.23 million NRSF. But the more important trend is deceleration. The forecast still shows new self-storage supply declining through 2027 and beyond. That matters because new supply pressures rents, occupancy, and lease-up timelines. For buyers, the right question is not, 'Is storage still viable?’ The right question is, 'How much new storage is hitting this exact trade area?’. Storage is a hyper local business with 70% of renters coming from a 10 minute drive area from the facility. There used to be a “if you build it, they will come” mentality with self storage development. That’s not the case anymore. Many developers have been burned by fast and loose underwriting resulting in slow lease up. Even seasoned developers that did their homework pre-development have felt the impact as additional developments sprout up agnostic of supply and demand, tanking the entire trade area. Construction costs have risen significantly bringing pause to many builders who relied upon cheap materials and quick build times, especially in the southern regions of the US. Most of the already zoned, flat land in high population areas has been gobbled up. Municipalities are placing moratoriums on new storage after a glut of development in the late twenty-teens and early 2020’s. These realities have cause the self storage supply pipeline to slow but certainly not stop.

Why do independent self storage owners still matter?

The big operators are everywhere, but they do not own the whole industry.

The five largest operators account for 19.3 percent of facilities and 35.6 percent of rentable square footage. That leaves a very large independent market. In fact, owners outside the top 100 still represent 66.4 percent of facilities and 37.3 percent of rentable square footage. That fragmentation is why acquisitions remain such a major opportunity. Buyers can still find assets where professional management, revenue management, better websites, call tracking, and local marketing can move performance. For owners thinking about selling, fragmentation also means buyers are actively looking for well-located properties with clean financials and upside. One of the best strategies in self storage is aggregation. Another way to describe this same strategy is defragmentation. Smaller operators can buy individual self storage facilities and package multiple together to form portfolios for larger operators to buy. One of the biggest downsides to self storage is that it’s comparatively difficult to deploy capital. In multifamily, you can buy a single 500 apartment, Class-A complex and drop tens of millions of dollars, if not hundreds of millions of dollars easily. In self storage, even the largest of self storage facilities top out below $50 million. This difficulty in deploying large amounts of capital is a road block to large private equity groups and REITs. The biggest of players need to resort to acquiring other large operators to get the scale and volume necessary. Buying from independent operators- mom and pop owners that have 2 or less facilities- and accumulating regional portfolios of self storage, creates a more attractive product as a result of appeasing the desire to deploy larger check sizes. Just by aggregating these independent facilities, a premium is applied as a result of the scale of investment. We find that a 20% plus premium is possible just by aggregating individual facilities into a larger portfolio. As the larger operators accumulate more of the independent facilities, the self storage industry becomes less fragmented.

How big is the self storage industry?

Self storage is not a niche side business anymore. It is a multi-hundred-billion-dollar real estate sector.

The U.S. self-storage industry is estimated at approximately $394 billion. The 2026 Self Storage Almanac also identifies 65,000-plus active facilities in the United States, more than 2.4 billion square feet, and over 3,900 known developments nationwide. That matters because scale changes how investors should think about the asset class. This is not just rows of garage doors. It is a national operating business with local demand drivers, fragmented ownership, pricing software, call handling, digital marketing, supply pipelines, and cap-rate discipline. For high-net-worth investors, the opportunity is not merely buying storage. It is buying cash-flowing businesses, that are also real estate, where operational improvement dramatically changes value immediately. Those elements have led to a lot of interest from big money, making this once small asset class one of the fastest growing.

How do I invest with SSSE?

At SSSE, we provide both accredited and non-accredited investors access to tax-advantaged self storage investments with an emphasis on downside mitigation and social stewardship. Our syndications range from acquiring existing value-add self storage facilities to expanding existing facilities, from converting vacant big box stores into self storage to building from the ground up.

At SSSE, we provide both accredited and non-accredited investors access to tax-advantaged self storage investments with an emphasis on downside mitigation and social stewardship. Our syndications range from acquiring existing value-add self storage facilities to expanding existing facilities, from converting vacant big box stores into self storage to building from the ground up. The first step to investing with SSSE is to fill out our investor onboarding webform. It is quick and easy and can be found on our website SSSE.com by clicking the “Investors” menu link in the upper left corner. Once you have submitted your investor webform, you will have the opportunity to schedule an introductory phone call with one of our investor relations team members. A scheduling program will automatically appear. After that, stay tuned for the next investment opportunity! If we have any active raises occurring that are a good fit for your investor profile, our investor relations team member will let you know on the call and will walk you through getting access to the investor portal. Otherwise, we typically will send out an email whenever there is a new investment opportunity. It will have the high level details including whether it is a 506(b) syndication (for both accredited and non-accredited investors that we have pre-existing relationships with) or a 506(c) syndication (for accredited investors only). There will also be a link to the investment opportunity’s web page! On the webpage will be more details including a short description at the top, followed by buttons to schedule a call, access the investor portal to review the documents, and a video summary. The investment process concludes with accessing the investor portal and signing the subscription documents and wiring funds through the investment portal. Our investor relations team will be there to help every step of the way.

What is an accredited investor?

Only accredited investors can invest in 506(c) syndications. We do both 506(b) and 506(c), so if you’re not yet an accredited investor, if you invest in enough of our 506(b) offerings, you’ll be headed in the right direction. The Securities and Exchange Commission sets the definition of an accredited investor.

Often we get asked, what is an accredited vs. a non-accredited investor. We get asked this because only accredited investors can invest in 506(c) syndications. We do both 506(b) and 506(c), so if you’re not yet an accredited investor, if you invest in enough of our 506(b) offerings, you’ll be headed in the right direction. The Securities and Exchange Commission sets the definition of an accredited investor. The definition is subject to change but as of the time of this writing, an accredited investor is someone who meets one of the following 3 requirements. 1. Income. You can be considered an accredited investor if you have a sustained annual income of at least $200,000 as a single investor, or $300,000 total if combined with a spouse’s income. 2. Professional. If you hold a valid Series 7, 65, or 82 license OR are a “knowledgeable employee” of certain investment entities. 3. Net Worth. Excluding the value of your primary home, if you have a net worth of $1 million or more, by yourself or combined with your spouse, you qualify to be an accredited investor. A couple reminders: part of the 506(c) syndication investment process will be verifying that you are an accredited investor, so “fake it til you make it” does not apply. Lastly, I am not an attorney or investment advisor. This information is purely for educational purposes. Please consult your legal and financial counsel for any questions, guidance, or advice.

How does SSSE underwrite properties?

Self Storage Syndicated Equities is committed to downside mitigation. Our underwriting process is our first step in minimizing risk. From the very first phone call or email we receive with an opportunity, there are at least 3 levels of underwriting that a deal must make it through prior to any consideration of investment.

SSSE is committed to downside mitigation. Our underwriting process is our first step in minimizing risk. From the very first phone call or email we receive with an opportunity, there are at least 3 levels of underwriting that a deal must make it through prior to any consideration of investment.

The first is our “back of the napkin” underwriting. Our acquisition team is fielding constant responses to our marketing efforts day in, day out. In order to be efficient and effective, they must collect a minimum threshold of information from a lead in order for it to be even considered an opportunity and continue to move through our process. That minimum information includes the contact information of the seller, broker, or wholesaler; the name and address of the property; size and/or acreage of the facility; current occupancy or zoning of the property; and current annual gross operating income.

With this information, we are able to identify an as-is financial valuation and replacement cost valuation for existing facilities. For development opportunities, we have standard build types that are possible based on the size of the lot and from that a range of value we can assign to the land with comparison to market value of similar listed and sold land. The purpose of the “back of the napkin” underwriting is to be able to provide an offer range as quickly as possible to the seller, broker, or wholesaler that will be fine tuned in later levels of underwriting.

If the lead passes our “back of the napkin” underwriting and becomes a potential opportunity, we perform our “underwriting lite”. This involves collecting readily available due diligence items and remaining information. Unit mix, pricing, expenses, recent capital improvements, needed capital improvements, management structure, build types, security components, insurance information, and more.

In our “underwriting lite”, we perform the “chicken pox test” on Google Maps, searching for storage in the nearby area to see how many red dots show in order to get a general sense of supply. We virtually drive the market using Google Street View to compare the subject facility to competitor facilities. We pull up census data to get a general understanding of population, trends, and demographics. We compare the subject facility’s unit prices to the 3 nearest competitor’s prices to see what sort of soft value add is available. We call the city building and zoning department to see if there are any active or applied permits for self storage development. Once we have completed underwriting lite, we should be able to solidify value and viability for the subject property. Beyond that, we have our full underwriting and analysis.

SSSE’s full underwriting and analysis takes all of the previous steps of our initial acquisition activities, formalizes them, and expands upon them. We have a full due diligence document checklist that the seller is required to submit prior to the due diligence period starting. We take all of the due diligence documents and audit them by recreating them within our standardized underwriting and analysis template. By auditing and recreating their rent roll, we are then able to create an accurate unit mix with each unit size’s range of rates accounted for.

In our full underwrite and analysis, we conduct an extensive competition study where we compare the supply index number, the competitors’ historic and current occupancy, and the subject facility’s historic and current occupancy in order to get an accurate assessment of the market’s supply and demand. The supply index number is determined by using satellite imagery and secret shopping to measure the size of each of the competitors and the type of storage the competitors provide. Using ArcGIS Esri Business Analyst we are able to map 1, 3 and 5 mile radii in addition to 5 minute, 10 minute, and 15 minute drive times, to establish our potential market and customer base. We analyze our potential market to determine population, income, housing and other metrics within the various radii. Dividing the population by the storage supply within our market radii provides us our supply index numbers which we compare against the state statistics provided by the latest Self Storage Almanac. Our competitor’s historic and current occupancy along with their unit rates is established through secret shopping. This underwriting triumvirate of supply index, subject facility occupancy, and competitor facility occupancy gives us as accurate of a market supply and demand study as possible. We are able to use the market supply and demand results along with the competitor unit rates matrix to determine what the market rates are and update the unit mix with the potential rental rates for each unit size.

By updating the seller’s unit mix with market rental rates gleaned from our competition study, we achieve a projection of gross potential income that can inform development and expansion plans. It allows us to project future years profit and loss in comparison to current income and expenses with downside mitigation factored in through stress tests, applying a range of decreases to income and an increases to expenses. We explore the various debt and equity structures available and the effects on cash after debt service and internal rate of return. Beyond the quantitative analysis, we collect qualitative information: physical appearances, amenities, opportunity zone qualifications, property insurance qualifications, FEMA flood map reference, police reports, and more. We order a Phase I Environmental Site Assessment, a Property Condition Assessment, drone photography, and a site walkthrough. In the scenario of an expansion, adaptive re-use, or ground up development, we order a third party feasibility study to verify our work and further mitigate downside risk for us and our investors.

When everything is said and done, we can identify if there are any changes needed to the purchase price, projections, or structure of each deal.

How much does a drive up self storage facility cost to build?

The cost to build a non-temperature controlled, drive-up self storage facility is going to be one of the cheapest ways to build self storage, only more expensive than portable units. Self storage is primarily made of steel and concrete, with steel being a highly traded commodity susceptible to supply chain disruptions, geopolitical factors, and economic events. As a result, the cost to build any type of self storage can vary greatly from location to location, month to month. As of the time of this writing, we have seen the cost of non-temperature controlled, drive-up self storage range from $40 to $60 per square foot. Decisions like compacted gravel vs. asphalt vs. concrete for drive aisles will increase prices. Temperature controlled, drive-up self storage is increasingly popular but is more expensive because of the HVAC systems, increased utility costs, and the loss of rentable square footage for utility closets. The trade off is the potentially higher rental rates that temperature controlled units garner. Renters often like drive-up units because of the convenience of being able to load and unload directly at the unit opening.

How much does a ground up development cost to build?

The cost to build a multi-story, temperature controlled, self storage facility is going to be one of the most expensive ways to build self storage. Self storage is primarily made of steel and concrete, with steel being a highly traded commodity susceptible to supply chain disruptions, geopolitical factors, and economic events. As a result, the cost to build any type of self storage can vary greatly from location to location, month to month. As of the time of this writing, we have seen the cost of building a class-A, multi-story, temperature controlled self storage facility range from $75 to $125 per square foot. Decisions like how many stories, how many elevators, smart locks, etc. will increase prices. There are ways to reduce costs like prefabricated components that are flat shipped and assembled on site. Involving your general contractor in the equity stack and incentivizing price reductions through a profit share structure can help ensure the best price and timely performance. We believe in getting multiple bids on every job.

How much does an adaptive reuse/conversion project cost to build?

The cost to do an adaptive reuse or conversion of a building into self storage is often less than the cost of building ground up. By using an already existing shell or “envelope”, you can reduce expenses dramatically depending on the condition of the shell. Self storage is primarily made of steel and concrete, with steel being a highly traded commodity susceptible to supply chain disruptions, geopolitical factors, and economic events. As a result, the cost to build any type of self storage can vary greatly from location to location, month to month. However, with an adaptive reuse or conversion project, you are not as exposed to the price of concrete and steel because not as much is needed with the exterior shell already existing. As opposed to structural components, the steel will be used for framing out units. As of the time of this writing, we have seen the cost of adaptive reuse or conversion projects of turning a building like a former big box store into self storage fall in the range of $45 to $85 per square foot. The condition of the shell- the roof, walls, foundation, electrical, HVAC, and fire suppression system- will greatly effect the project cost. If the shell is not in good condition, there becomes a break even point of using the existing shell vs. building a new shell from the ground up. Some pre-existing buildings will have enough ceiling height to consider building a mezzanine second level which will effect not only the price of the build-out but also the potential revenue the footprint of a given building can generate.

How do you price or value a self storage facility?

We price a self storage facility based on 3 different methodologies: financial, replacement, and highest use. Financial valuation is the most common and widely used methodology since self storage is a commercial real estate asset and commercial real estate is typically traded based on capitalization rates or “cap” rates. Determining a cap rate is taking the capital deployment (i.e. the purchase price) and dividing by the net operating income. It results in a percentage, like an 8% cap rate.

Net operating income is calculated by the annual gross operating income- all of the revenue that a facility generates before expenses- and subtracting the annual expenses the facility experiences. This results in the net operating income figure or “NOI”. Debt servicing is not included in the expenses used for calculating net operating income. Once you have a net operating income, you can reverse calculate the value of a facility if you establish what the market cap rate is. If it’s a nicer facility in a nicer, more populous area, it will most likely trade for a lower cap rate and thusly a higher premium.

A different valuation methodology from financial is replacement cost. This methodology is often best used for severely underperforming facilities, recent builds, or facilities in lease up because their financial performance may not be an accurate assessment of its current or future value. For instance, if you spend $10 million building a beautiful ground up development of a Class A self storage facility, and it just received certificate of occupancy so it is 0% occupied, financial valuation of the facility would put it at a value of $0. Actually less than $0 because there are expenses like property taxes and insurance that make it a negatively performing financial vehicle. 3 years from certificate of occupancy when the facility is leased up and performing, it now can garner a financial valuation of higher than $10 million potentially. Replacement cost valuation looks at how much it would cost to rebuild a facility using current construction costs but factoring in the wear and tear that the subject facility has experienced. So in that same scenario that we just discussed of the $10 million dollar new build facility, a replacement cost valuation would account for it costing $10 million to build. But now, construction and land costs could be higher and the fact that its already built as opposed to having to go through planning, zoning, and construction, provides a premium, so the replacement cost valuation could be even more than $10 million and it could make sense for the owners to sell as-is instead of leasing it up for a financial performance valuation. That’s not to say that people don’t buy facilities based on pro forma, or the potential financial performance of a facility. We certainly agree that should be accounted for in any valuation methodology, but we are not of the mindset where we want to pay the previous owner for our future work dollar for dollar.

Besides the financial and replacement methodologies we use to price and value self storage facilities, there is the highest and best use methodology. One of the benefits of self storage is that it can be built in a number of ways. If you have an empty box, it can typically be filled with smaller boxes making self storage. Highest and best use takes a look at the current performance and use of a property and determines if there is a better use for the property that would result in better performance. For instance, this could be converting non-temperature controlled self storage into temperature controlled. It could be taking larger units and making them into smaller units by using dividing walls because there is pent up demand for smaller units in the market and the rental rate per square foot is higher with smaller units. The most common scenario is a warehouse that needs to be converted into traditional self storage lockers as opposed to a wasted open space that is inefficient in its rental potential. Or a vacant piece of land that could have self storage built on it. Vacant land is not the highest and best use of that parcel. By changing the use to the best use of a property, it can bring a higher value to the property.

With these three different valuation methodologies- financial, replacement, and highest use- we can accurately value any sort of self storage property. Stating the obvious, the highest price with the best terms will usually get the deal done. So we employ these three different valuation methodologies to determine which route will allow us to make our best offer with the highest chance of getting accepted.

What cap rates do self storage facilities sell for in 2023?

The subject of self storage facility cap rates is one that does not age well. The bottom line is that self storage is a commercial real estate asset that has performed the best out of all real estate asset classes through recessionary periods so while other cap rates may be negatively impacted in the upcoming years, we believe that self storage will fair the best. We approach self storage cap rates from a 9 category matrix. There are 3 types of markets and 3 grades of self storage. Primary markets, secondary markets, and tertiary markets. Primary markets are major cities with high population density. We categorize that as populations of 250,000 or greater within a 10 minute drive time. Secondary markets we categorize as populations of 75,000 people to 250,000 within a 10 minute drive time. Tertiary markets are anything below that and because of the smaller populations, the density is usually less and it causes the trade area to increase sometimes to a greater than 10 minute drive time.

Class A self storage is mostly found in primary markets but we are seeing it more and more in secondary markets as the REITs and other institutional players expand out of the saturated primary markets into secondary markets. Class A is going to be newer, more expensive build types, multi-story, and temperature controlled. Class B is going to be slightly older, a mix of multi-story and single story drive up, with amenities like paved aisles, automatic gates, and potentially temperature control. Class C is going to be pretty much everything else: older drive-up units, possibly unpaved with gravel, compacted substrate or hopefully not just mud and grass. It is not an exact science and there is the largest range of quality facility within Class C which prompts some groups to use additional letters.

As you can imagine, a Class A facility in a primary market is going to trade at the lowest cap rate meaning that it is valued the highest, with the highest premium paid by buyers. A Class A facility in a primary market is going to trade at a lower cap rate than a Class A facility in a secondary market because of the security that a greater population and hopefully corresponding demand provides. So the Class C facility in a tertiary market is going to trade for the highest cap rate, or the lowest premium, because it is not as pretty of an asset, with potentially more risk.

We love to buy existing Class C and Class B self storage facilities for value add investment where we can improve their performance or even improve their asset class categorization. We like to build Class A self storage facilities because the premium to buy is incredibly steep so we are able to build them for less than purchase, lease them up, and either refinance at stabilization or sell them to market at the premium that grade asset garners. Historically, we have seen Class A facilities in primary markets trade for as little as 3% cap rates as long as there is room for increasing the financial performance. Over the past 3 years, we have bought Class C facilities in tertiary markets for as high as 12% cap rates. The rest of facility class and market combinations fit within that range, but now cap rates are rising because of interest rates.

Cap rates typically float above interest rates because of cash flow needs. So with the drastic increases in interest rates over 2022, we are seeing cap rates for all self storage facility grades and locations slowly rise to meet the higher interest rates. There is a lag in cap rates increasing and it is not directly proportional to the interest rate hikes because self storage is such a highly desired real estate asset especially for its recession resilience. As a result, we are seeing the highest valued self storage facilities trading at above 5% cap rates at the start of 2023.

The relationship between self storage facility values and interest rates can boil down to debt service coverage ratio (DSCR). Debt service coverage ratio is the calculation of net operating income versus debt payments. If the net operating income and debt service costs are exactly the same, it would be a DSCR of 1. Lenders typically want to see a DSCR of at least 1.25 so there is a buffer between loan costs and revenue from the facility, meaning that the net operating income of a facility can more than cover the debt payments. So as the cost of real estate loans go up with interest rate increases, the value of self storage facilities and other commercial real estate can go down unless the net operating income also increases to maintain bank required debt service coverage ratios.

How much money do I need to invest as a syndication participant?

How much you need to invest as a syndication participant is dependent on the investment opportunity. The syndication sponsors set the minimum investment amount and communicate that to the potential investors. This can be as little as $25,000 but can be much higher. There is often a maximum investment amount as well in order for the syndication sponsors to protect ownership interest so that a single investor does not come in and take over a deal or break a threshold which would require an investor to be a loan guarantor based on their ownership percentage. Each of our syndications at SSSE has the minimum investment and maximum investment established on a deal by deal basis with our lowest minimum investment at $25,000.

How does SSSE act on its commitment to “social stewardship”?

Our company on-liner is “tax-advantaged self storage with an emphasis on downside mitigation and social stewardship”.

By nature self storage mitigates downside and is tax-advantaged. In the Great Recession of 2007-2009, self storage dropped -3.8% in comparison to the S&P 500’s -22%. This was the smallest drop of any real estate asset class. From 2011-2018, self storage had the lowest default rate of any real estate asset class. When those rare few properties did default, the banks only lost an average 1.52% per default. Banks recognize the inherent downside mitigation of self storage and that’s why its one of their favorite assets to lend on.

We further emphasize downside mitigation with our rigorous underwriting and analysis. Each of our syndications and investments is required to have multiple exit strategies. With our robust pipeline of leads and opportunities, we are never in a position where we feel the need to take on a new acquisition or development because of pressure to deploy capital. We pick the best opportunities to move forward with when it makes sense to do so.

As for tax advantages, the government provides incentives for anything that creates food, jobs, or shelter. While self storage is not housing, it is real estate and has all of the great tax benefits like bonus depreciation. We consider tax benefits as part of our analysis process, and choose deals that will result in the greatest tax benefits.

Our company one-liner emphasizes social stewardship. We believe that self storage can be more than metal boxes. We are very fortunate with the opportunities that self storage affords us. One of those is the opportunity to give back to the communities our storage facilities serve and to make environmentally conscious decisions when designing our developments. Energy efficient materials, solar panels, electric vehicle chargers, green roofs, native species landscaping, and more are all considerations we take into account when planning and designing our new self storage facilities. Our primary focus in regards to social stewardship is participating and donating to local charitable causes for each of the communities our storage facilities serve. Self storage is an incredibly localized business. On average, 70% of renters come from a 3 mile radius of a self storage facility. This is an opportunity for us to really participate in our communities. Our charitable donations and participation is focused around food, shelter, and jobs. Some of our most common avenues for giving back to the areas we serve are local food banks, domestic violence shelters, and after school programs. Our renters trust us to store and protect their beloved belongings, and we want to go beyond that to protect and improve the communities that store our properties.

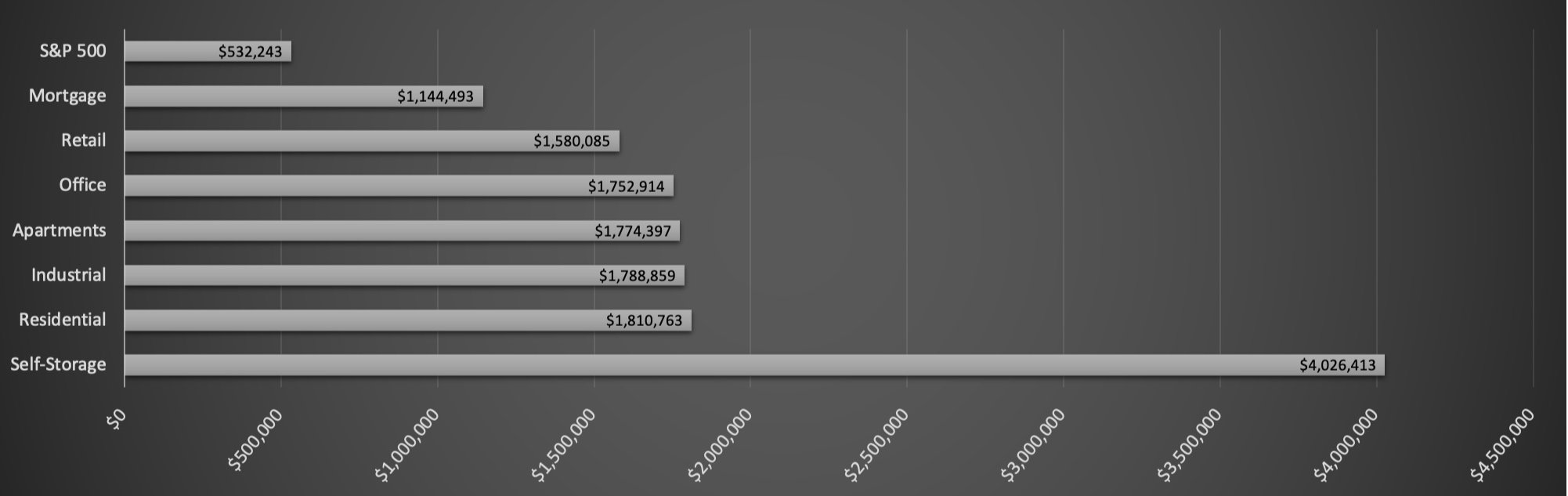

How does self storage compare to other real estate assets in regards to return on investment?

Self storage has the highest return on investment in comparison to any other real estate asset class. From 1994-2017, storage returned an annual average of 17.43%. Based on that annual average, $100,000 invested in 1994 would be over $4,000,000 as of 2017. In comparison, if you invested in apartment buildings over that same time, the $100,000 would be $1,774,397 as of 2017.

2017 Value of $100,000 Invested in 1994 Based on Average Annual Return by REIT Sector

Is self storage recession resilient?

From 2007-2009, self-storage dropped -3.8% in comparison to the S&P’s -22.0%. This was the smallest drop of any real estate asset class. Self storage had some of its best performing years during the COVID-19 Pandemic when some other real estate asset classes performed poorly. According to Trepp, a Commercial Mortgage Backed Securities research firm, of the 1,700 CMBS loans made to self storage in the first 3 quarters of 2020 only 3 were delinquent– that is a 0.17% delinquency rate . During the same time multi-family was defaulting at a rate 1,800% higher or 18x that of self storage.